Time to make cigarette taxes more effective in Mozambique

Introduction

Research has shown that the two most important determinants of the demand for cigarettes is the price of the product and people’s incomes. The two measures combined determine how affordable cigarettes are. The affordability measure used by the World Health Organization (WHO) is the percentage of per-capita gross domestic product (GDP) required to purchase 100 packs of cigarettes per year. If this percentage increases, it means that more resources are required to purchase a given quantity of cigarettes, and thus cigarettes become less affordable. Similarly, if this percentage decreases, fewer resources are required to purchase a given quantity of cigarettes, and thus they become more affordable.

Cigarette affordability is an important measure of the effectiveness of tobacco taxes. According to the World Bank Group, tobacco prices in Mozambique increased by 27% in real (inflation-adjusted) terms between 2013 and 2016, while real per-capita GDP increased by 14% over the same period. This means that cigarette prices rose faster than the increase in income, making them less affordable. The current excise tax is adjusted by approximately 4% per annum in nominal terms in Mozambique. Between 2022 and 2023, the cigarette excise tax is predicted to increase by 19%, and then increase by approximately 4% per annum between 2023 and 2027[1] in nominal[2] terms.

A key measure of the efficacy of tobacco taxes is the change in cigarette affordability. The Tobaconomics cigarette tax scorecard, which keeps track of global cigarette tax developments, scored Mozambique well on the indicators of affordability and tax structure in 2020. It scored very poorly on the share of tax in the retail price, and on cigarette prices (which, for the Score Card, are expressed in international dollars and are relatively low in Mozambique compared with other African countries). (See Table 1). With the exception of Malawi, all neighbouring countries (Eswatini, South Africa, Zambia, and Zimbabwe) have cigarette prices and taxes much higher than Mozambique. An effective tax increase would result in increased excise revenue and reduced demand for cigarettes.

Tobacco taxes in Mozambique

Mozambique currently has a uniform specific excise tax of 8.40 Mozambican Meticais (MZN) per pack of 20 cigarettes (approximately USD 0.13). A uniform specific tax means the same tax rate is used across different cigarette brands; this is considered best practice. As a percentage of the retail selling price (RSP) of the most sold brand (MSB), the excise tax comprises only 12.4%, while the current total tax share (which includes the value-added tax or VAT) accounts for 25% . The WHO recommends that the excise tax should comprise at least 70% of the retail price, or the total tax share should account for 75% of it. Mozambique’s current tax shares are among the lowest in the Southern African Development Community (SADC) region, with the exception of Angola. At the other extreme is Mauritius, with an excise tax share of 71% and a total tax share of 84% of the price of the most sold brand. The average excise tax share and total tax share of the retail price of the most sold brand stood at 37% and 52%, respectively, in 2020 for the SADC region.

Moreover, cigarette prices in Mozambique are much lower than in the neighbouring countries, as Table 1 shows.

Table 1: Excise and total tax share in price of a pack of the most sold brand (MSB) of cigarettes, 2020, selected SADC countries

|

Country |

Excise tax share (%) |

Total tax share (%) |

Price of MSB |

Affordability |

|

|

International USD (purchasing power parity[3]) |

Price in USD official exchange rates |

% of GDP per capita required to purchase 100 packs of the MSB |

|||

|

Angola |

3 |

12 |

5.49 |

1.56 |

7.9 |

|

Botswana |

35 |

52 |

10.84 |

4.31 |

6.7 |

|

Eswatini |

40 |

54 |

6.44 |

2.57 |

7.2 |

|

Lesotho |

38 |

51 |

7.81 |

2.77 |

27.1 |

|

Madagascar |

64 |

80 |

3.52 |

1.05 |

21.4 |

|

Mauritius |

71 |

84 |

8.87 |

3.75 |

4.3 |

|

Malawi |

42 |

56 |

1.76 |

0.71 |

17.7 |

|

Mozambique |

14 |

29 |

2.46 |

0.85 |

19.2 |

|

Namibia |

29 |

42 |

8.26 |

3.58 |

8.7 |

|

South Africa |

40 |

53 |

6.45 |

2.62 |

5.4 |

|

Zambia |

25 |

39 |

3.91 |

1.16 |

11.8 |

|

Zimbabwe |

16 |

29 |

5.75 |

1.24 |

18.4 |

Source: WHO Global Tobacco Control Report, 2021. Table 9.1 and Table 9.6.

We used the Tobacco Excise Tax Simulation Model (TETSiM), designed by the Research Unit on the Economics of Excisable Products (REEP), to simulate the impact of different excise tax changes on cigarette tax shares (expressed as a percentage of the selling price), cigarette demand, cigarette tax revenue, and the adult smoking prevalence rate, between 2023 and 2027, using 2022 cigarette excise tax rates as the baseline. We present our results in constant 2022 prices.

Methods and assumptions

The cigarette market in Mozambique can be divided into four product segments: imported, popular, economy, and illicit. Based on information from the Mozambican customs authority, the illicit market accounts for about 5% of the total cigarette market share in Mozambique.

Two crucially important inputs are the price and income elasticities of demand. The price elasticity of demand quantifies the relationship between a change in the real (i.e. inflation-adjusted) price and demand. Based on a large international literature, we used price elasticities that range from -0.6 to -0.8, implying that a 10% increase in the price of cigarettes results in a fall in demand by between 6% and 8%.

Similarly, the income elasticity of demand measures the change in demand in response to a 1% change in income. Most estimates of income elasticity of demand for tobacco products lie between 0 and 1. We assumed that the income elasticities for demand for legal cigarettes range from 0.3 to 0.5, and -0.5 for illicit cigarettes. This means that a 10% increase in real per-capita GDP (the proxy for income that we use in the model) is expected to increase cigarette demand for legal cigarettes by between 3% and 5%, and reduce the demand for illegal cigarettes by 5% (see Table 2). Implying that, for example, smokers would increase the number of legal cigarettes smoked per day (smoking intensity) as cigarettes become more affordable to them, following an income (GDP per-capita) increase, if all other factors remain unchanged.

If particular brands become more expensive, some people will switch to cheaper brands. The concept that describes and quantifies the switching behaviour is the cross-price elasticity of demand. Within the context of this model, the cross-price elasticity of demand is the percentage change in the demand for the cheaper market segment in response to a 1% increase in the price of the more expensive market segment. Although it makes intuitive sense that this type of switching happens, there is currently not a large empirical literature that quantifies the cross-price elasticity of demand. We used cross-price elasticities that range from 0.05 to 0.10 (see Table 2).

Table 2: TETSiM input data

|

Input variables |

Imported |

Popular |

Economy |

Illicit |

|

Market share |

2% |

51% |

42% |

5% |

|

Retail price (current MZN) |

155 |

68 |

40 |

20 |

|

Retail price (current USD) |

2.40 |

1.05 |

0.62 |

0.31 |

|

Specific excise tax (current MZN) |

8.4 |

8.4 |

8.4 |

0.00 |

|

Specific excise tax (current USD) |

0.13 |

0.13 |

0.13 |

0.00 |

|

VAT |

17% |

17% |

17% |

0% |

|

Income elasticity |

0.50 |

0.40 |

0.30 |

-0.50 |

|

Price elasticity |

-0.6 |

-0.70 |

-0.80 |

-0.80 |

|

Cross-price elasticity |

. |

0.05 |

0.10 |

0.10 |

|

Excise tax share of retail price |

5.4% |

12.4% |

21.0% |

0.0% |

|

Total tax share of retail price |

31.8% |

25.0% |

34.2% |

0.0% |

Global evidence suggests that the impact of a price increase impacts about half on prevalence and half on smoking intensity (number of cigarettes smoked per day). We use this evidence to estimate the impact of a cigarette tax increase on the adult smoking prevalence rate.

In order to simulate how an increase in the cigarette excise tax share compares with those of other countries in the SADC region, and its effect on the current cigarette prevalence rate, two scenarios were considered. In the first scenario, the status quo scenario, we assume that the adjustments to the cigarette excise taxes remain as stipulated in the current cigarette excise tax schedule for 2022 to 2027, that is, increase by 19% between 2022 and 2023, and then increase by approximately 4% per annum between 2023 and 2027. We compare this scenario with a scenario where Mozambique would follow the WHO FCTC Article 6 guidelines, which recommend adjusting the specific excise tax annually in line with both inflation and income growth. This scenario proposes a 30% annual increase to the current excise tax rate over and above the recommended annual inflationary and income adjustments. We recommend this additional 30% annual increase in order to account for the current low cigarette excise taxes in Mozambique and increase the excise tax and total tax shares of the selling price. We refer to this simulation as Scenario 2. We used GDP per capita as a proxy for income. In both scenarios, we assume an over-shift[4] of the tax by between 12% and 15%[5] as the industry in Mozambique is relatively concentrated with three multinational tobacco companies, of which one, British American Tobacco, accounts for over 90% of the market. In cases of highly concentrated markets, industries are likely to over-shift the tax.

TETSiM results

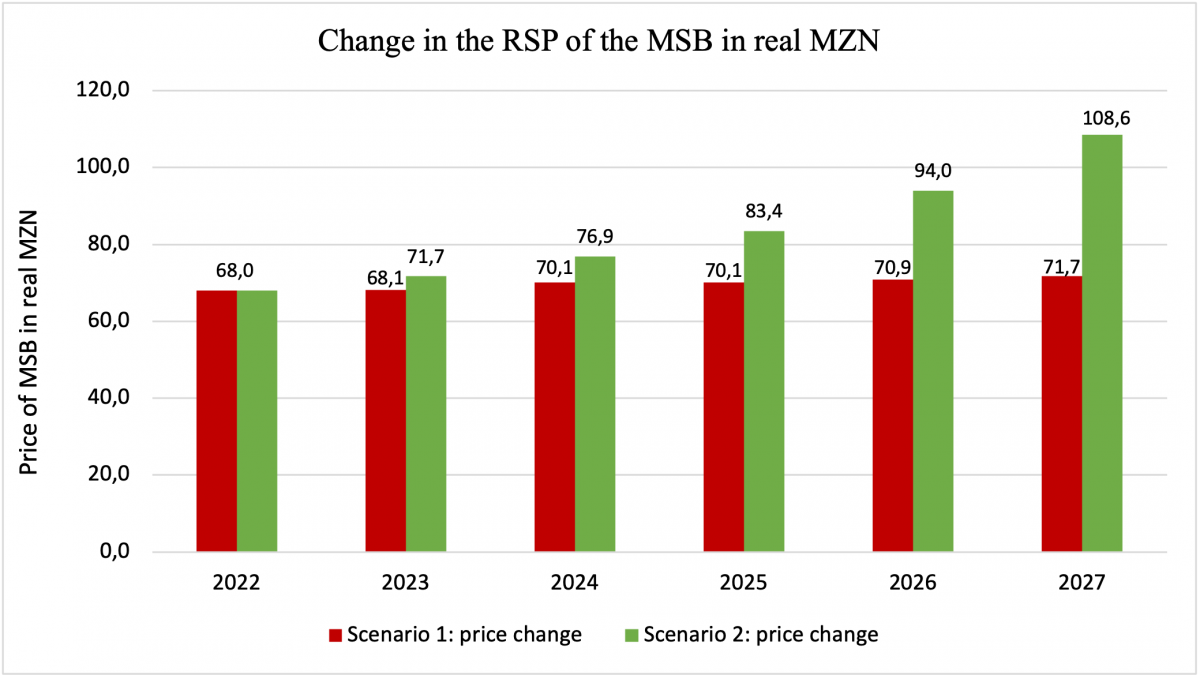

Scenario 1 results in the retail price (RSP) of the most sold brand (MSB) increasing from 68 MZN in 2022 to 71.7 MZN in real 2022 prices between 2022 and 2027, a 5.5% increase. For scenario 2, the retail selling price of the most sold brand increases from 68 MZN to 108.6 MZN during the same period, a 60% increase. (See Figure 1).

Figure 1: Change in the retail selling price of the most sold brand (MSB) in real MZN

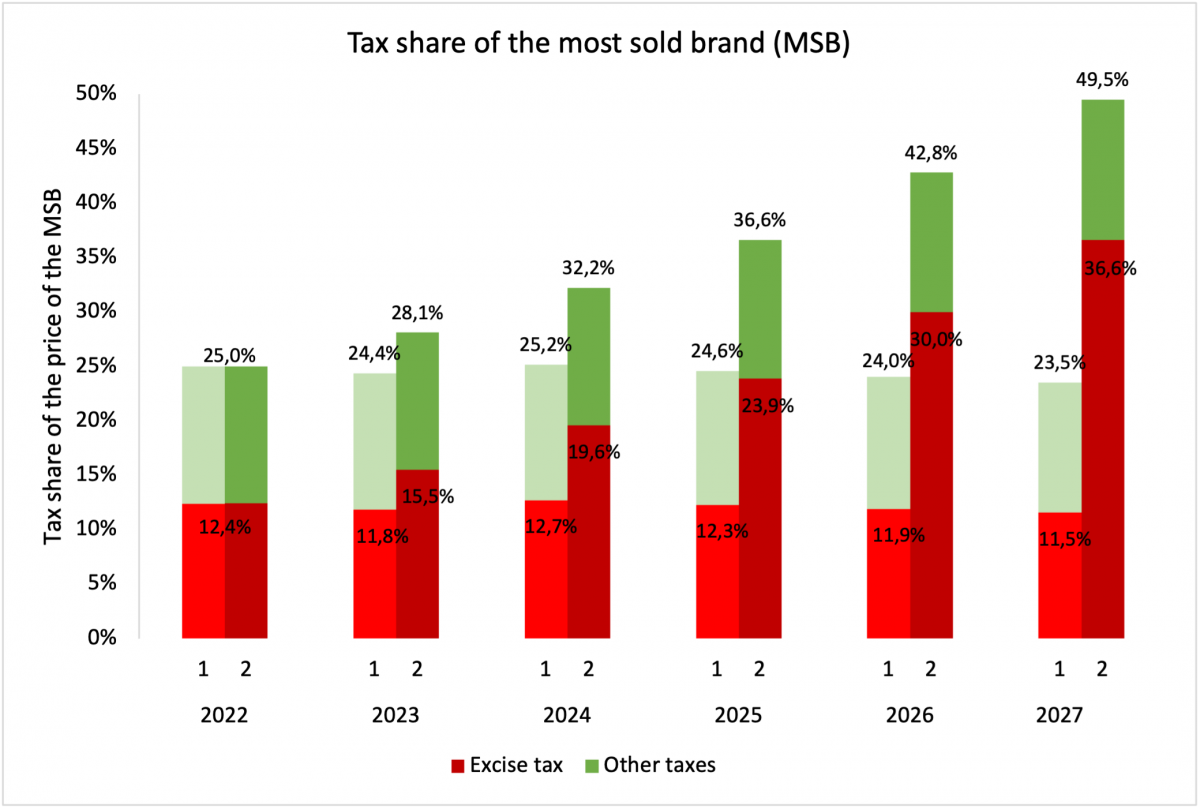

Our results show that under Scenario 1, the excise tax share will drop from 12.4% in 2022 to 11.5% of the retail selling price by 2027, and the total tax share will drop from 25% to 23.5% of that price in the same period. However, the simulation results for Scenario 2 suggest that the real uniform specific excise tax per pack would increase from 8.4 MZN in 2022 to 39.78 MZN by 2027. The excise tax share of the retail price of the most sold brand would increase from 12.4% in 2022 to 36.6% in 2027. The total tax share of the most sold brand would increase from 25% in 2022 to 49.5% of the price by 2027 (see Figure 2.)

Figure 2: The excise and other tax share of the retail price of the most sold brand

1= Scenario 1 , 2= Scenario 2.

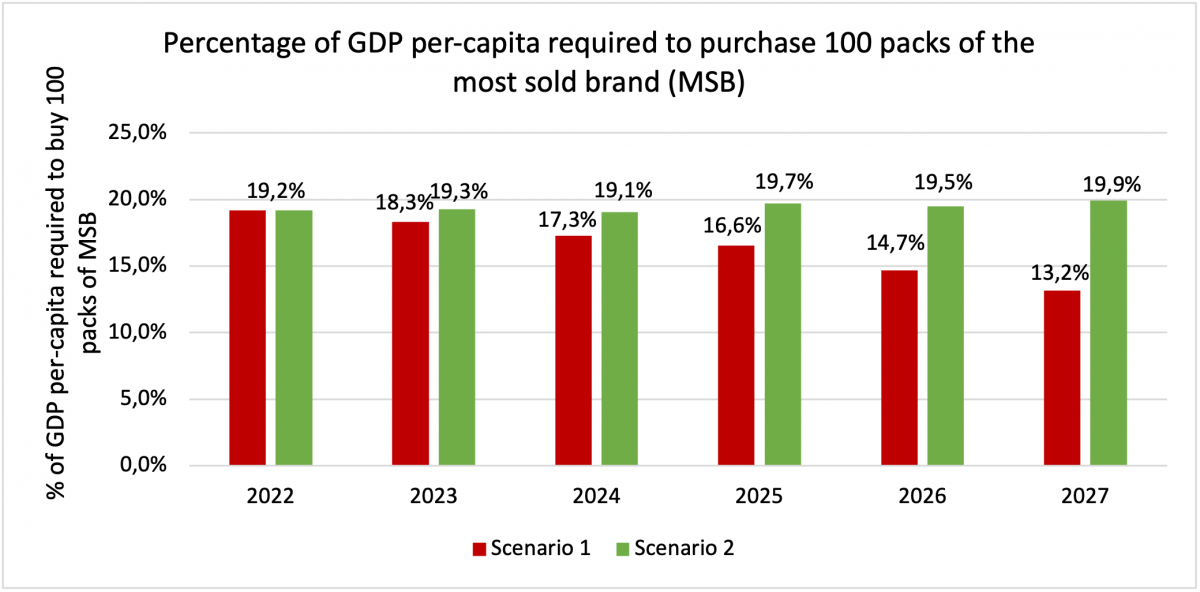

In Scenario 1, cigarettes would be expected to become more affordable over time, with the percentage of per-capita GDP required to purchase 100 packs of the most sold brand dropping from 19.2% in 2022 to 13.2% by 2027. However, in Scenario 2, cigarette affordability remains relatively unchanged, increasing from 19.2% of the GDP per-capita required to purchase 100 packs of the most sold brand in 2022 to 19.9% by 2027 (see Figure 3).

Figure 3: Change in affordability of the most sold brand

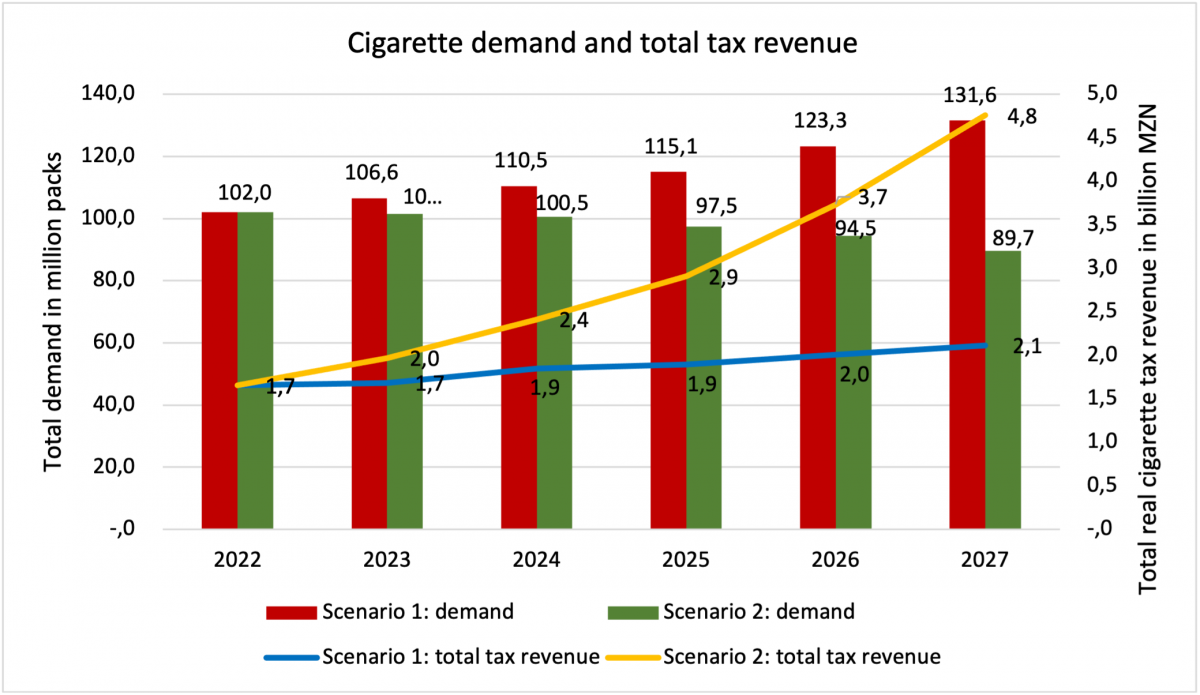

Per-capita GDP is predicted to grow rapidly in Mozambique, which would counteract some of the demand-reducing consequences of the excise tax increase. Scenario 1 would result in a 29% increase in the demand for legal[6] cigarettes between 2022 and 2027, whereas Scenario 2 is expected to result in a 12% decline in legal demand (see Figure 4). In Scenario 1, the total cigarette tax revenue increases by 28%, from 1.7 billion MZN to 2.1 billion MZN by 2027 in real (inflation-adjusted) values. In Scenario 2, the total cigarette tax revenue increases by 188% from 1.7 billion MZN in 2022 to 4.8 billion MZN by 2027 in real values. Despite the fall in demand in Scenario 2, total cigarette tax revenue increases because the drop in demand is much smaller than the increase in the excise tax per cigarette.

Figure 4: Total legal cigarette demand in million packs and total real tax revenue in billion MZN

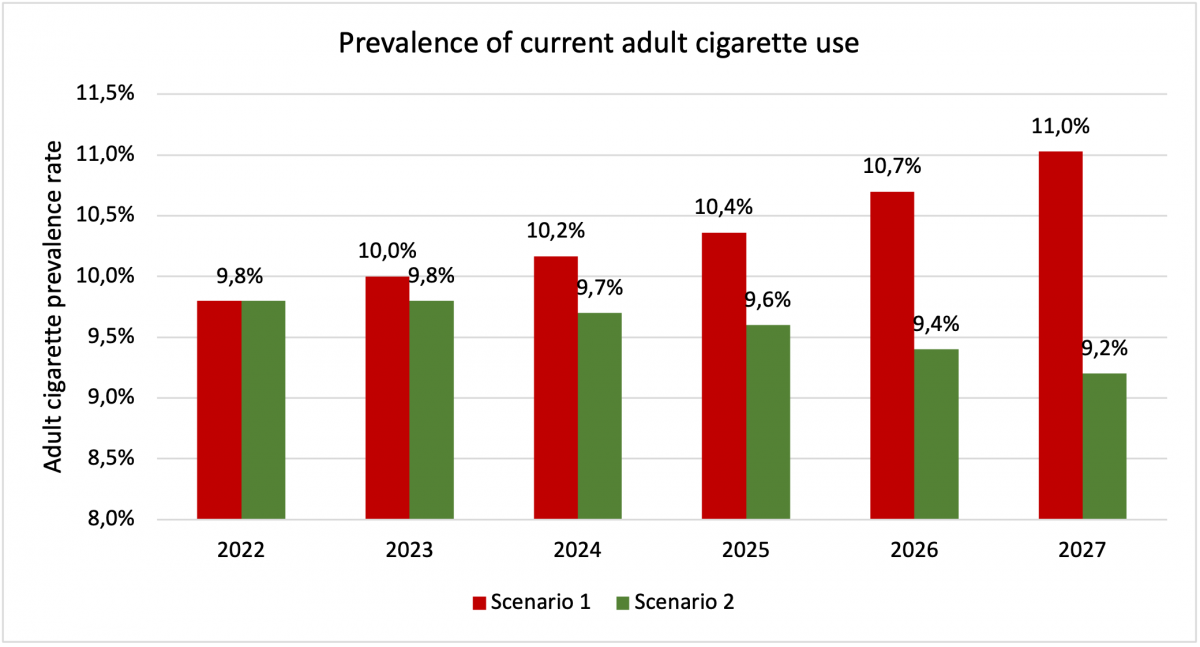

Our results suggest that the adult cigarette smoking prevalence rate will increase from 9.8%[7] to 11% between 2022 and 2027 under Scenario 1. However, under Scenario 2, the adult cigarette smoking prevalence rate is expected to decline from 9.8% to 9.2% in the same period (see Figure 5).

Figure 5: Change in the adult cigarette smoking prevalence rate

Policy recommendations

We recommend that the Mozambican government adjust the cigarette excise tax annually by at least 30% over and above the sum of the GDP growth rate and inflation rate. This will result in:

- an increase in the cigarette excise tax per cigarette;

- an increase in the excise tax and total tax shares of the selling price;

- a reduction in the affordability of cigarettes;

- a reduction in the demand for cigarettes;

- an increase in cigarette tax revenue, over time, while simultaneously making cigarette prices and tax shares in Mozambique comparable to prices and cigarette tax shares in the southern African region.

Furthermore, a more aggressive excise tax will result in a decline in cigarette smoking prevalence, and the associated harms of tobacco use.

[1] Based on personal communication between REEP and WHO Mozambique

[2] An increase that does not take inflation into account.

[3] A currency conversion to equalise the purchasing power of the different currencies, by eliminating the differences in price levels between these countries.

[4] An over-shift is when the industry increases the retail price by more than the tax increase.

[5] We used an over-shift of 15% for the imported, and popular segments, 12% for the economic segment and 25% for illicit segment in both scenarios.

[6] We illustrate the changes to legal cigarette demand as only legal cigarettes are subject to cigarette taxes.

[7] The age standardized current cigarette smoking rates among people aged 15 years and older in 2020.

Download article

Post a commentary

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. To comment one must be registered and logged in.

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. Please view "Submitting a commentary" for more information.